[ News & Updates ]

A practical breakdown of Uganda's Anti-Money Laundering Act and what the Financial Intelligence Authority (FIA) expects from regulated institutions, KYC, transaction monitoring and suspicious-activity reporting.

Picking a KYC vendor for an East African bank or fintech is harder than it looks. Seven questions to ask any KYC platform before you sign, registry coverage, latency, audit trail, pricing and hosting.

Financial institutions need to invest in a substantial anti-money laundering (AML) technologies to catch criminals, to meet compliance requirements, and to avoid the heavy penalties for failing to do so. AML screening helps financial institutions in Africa improve compliance.

Risk profiling and rating helps financial institutions assess the risk associated with new customers - both individuals and businesses. It helps banks make informed decisions about the level of due diligence required for each customer and ensures compliance with applicable laws and regulations.

Uganda-based fintech startup Laboremus has received further funding to accelerate the adoption of digital KYC and customer onboarding solutions in Africa.

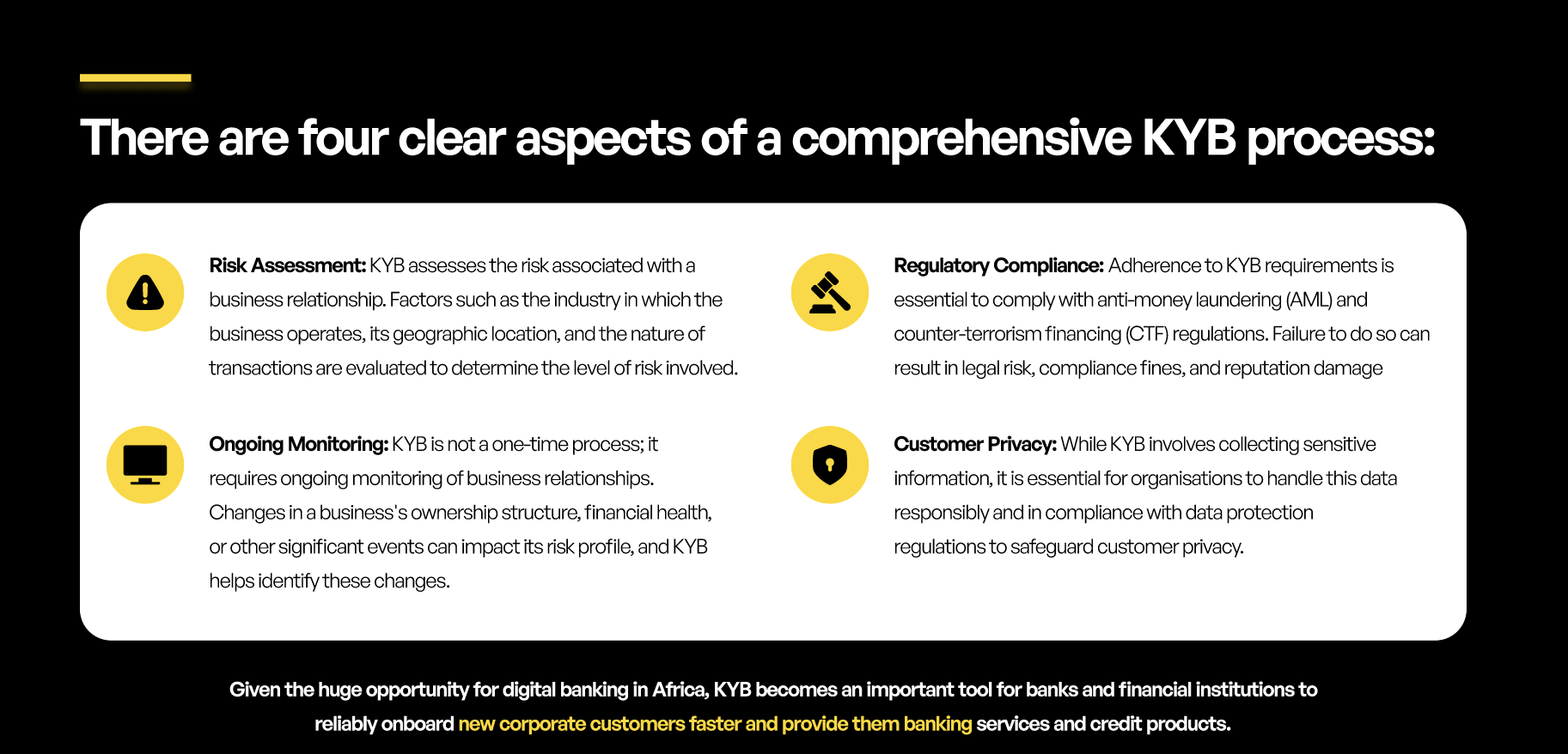

Automating KYB is a challenge for banks and financial institutions. There are many hurdles that need to be overcome. Laboremus has automated the KYB process for banks and financial services companies in Africa.

Politically exposed persons (PEPs) pose a higher risk of corruption and involvement in money laundering and/or terrorist financing. To mitigate the potential risk, financial regulators require financial institutions in Africa to implement enhanced due diligence (EDD) measures and clearly identify PEPs. Here we summarise key considerations for financial institutions and banks to build a reliable PEP due diligence process.

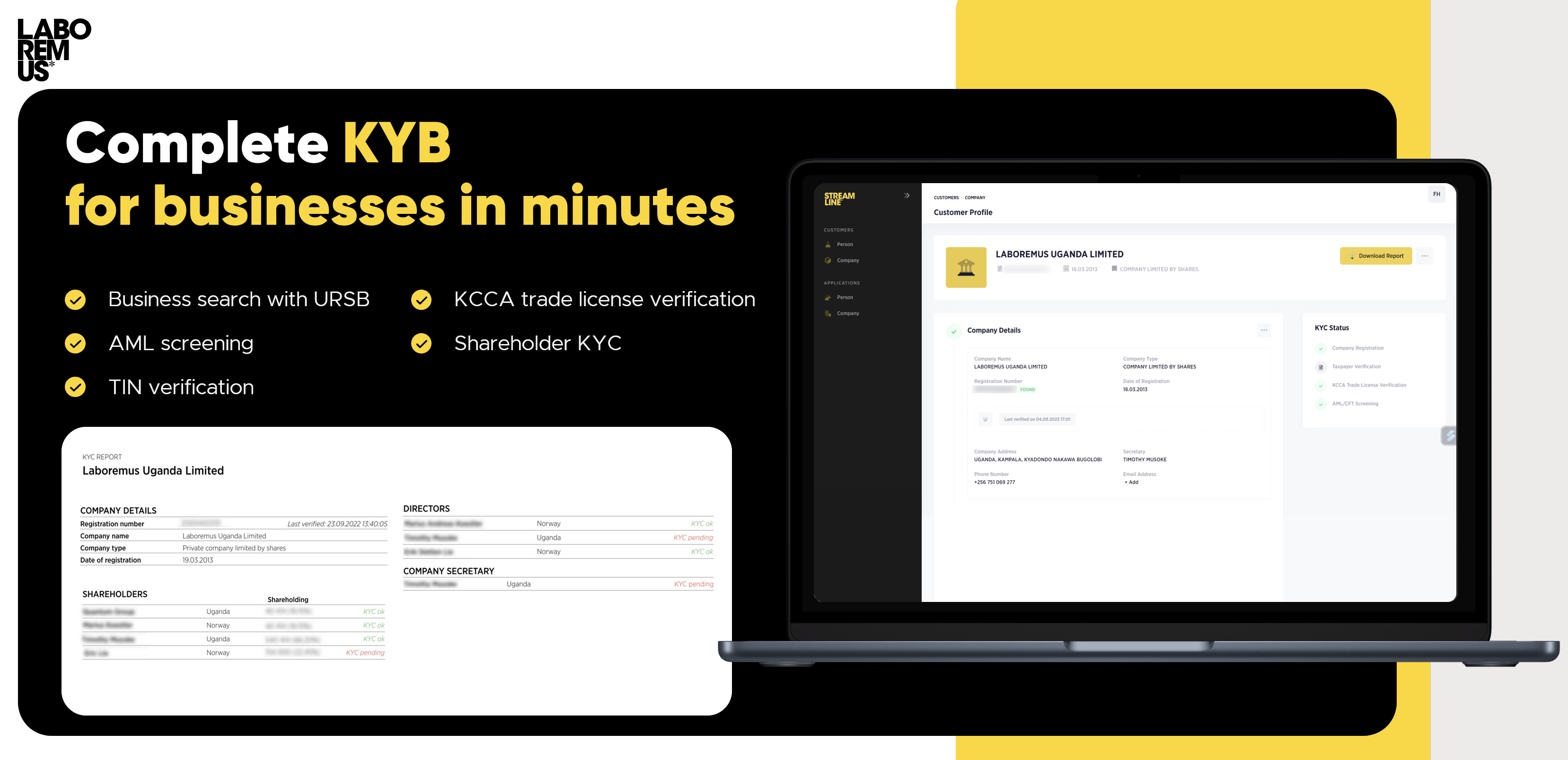

A deep dive into KYB for banks and financial institutions in Africa. KYB is essential for financial institutions to verify the identity and legitimacy of their business partners, customers and suppliers.

As adoption of digital banking accelerates in Africa, financial institutions are quickly running into the limits of their existing infrastructure. We explore how legacy infrastructure disrupts growths for banks in Africa and how using Middleware solutions can accelerate your digital transformation journey.

ADC, Rabobank Foundation and Laboremus Uganda are happy to announce a partnership to help Uganda’s dairy farmers and cooperatives grow.

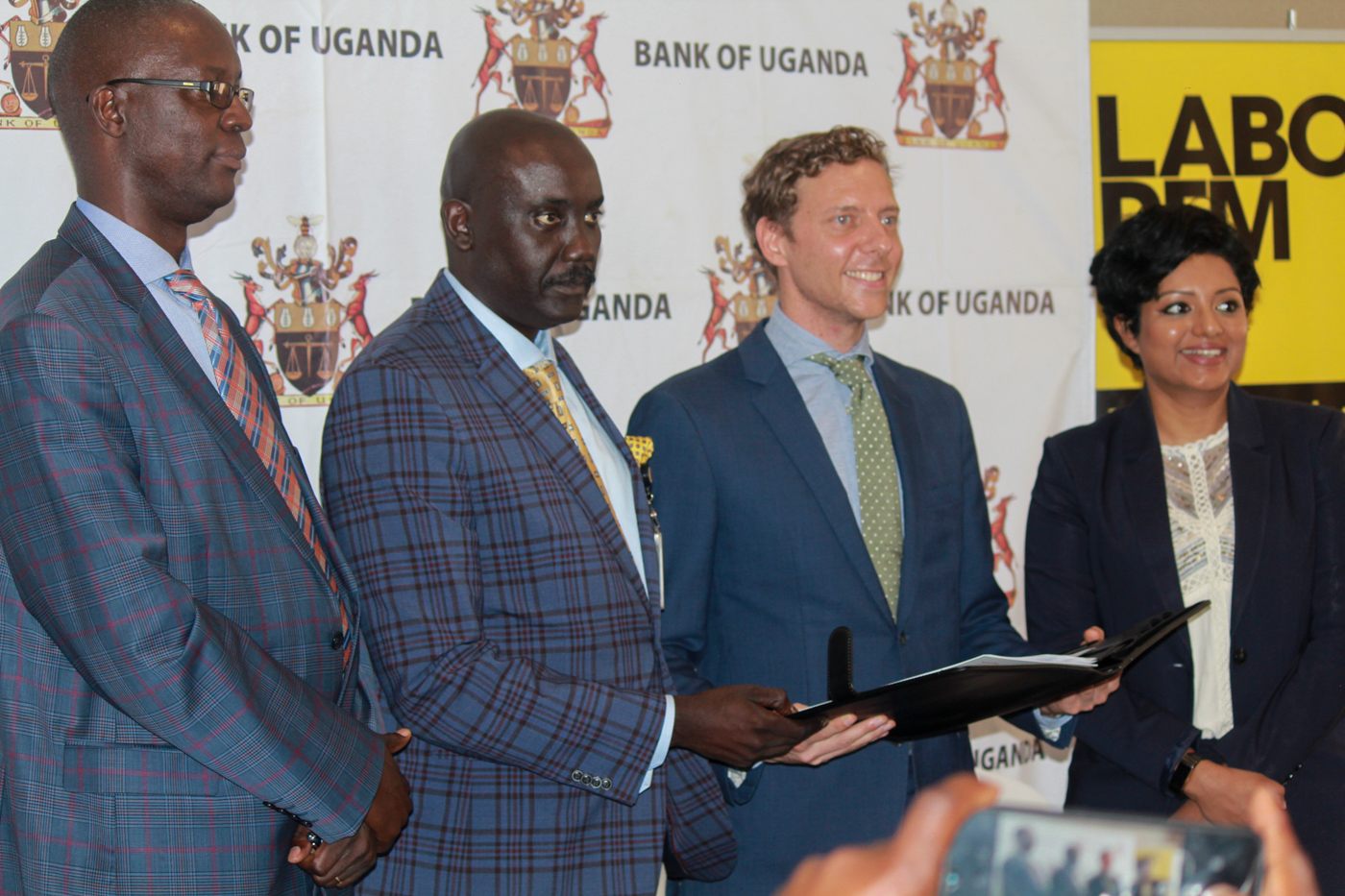

Bank of Uganda (BoU), in collaboration with Uganda Bankers’ Association (UBA) and Financial Sector Deepening Uganda (FSDU) have signed a contract with fintech company Laboremus Uganda to develop a digital ID verification system to be used by all banks and other licensed financial service providers in the country.

Financial crimes pose a significant concern for financial institutions, and organizations are obligated to comply with anti-money laundering regulations to combat such crimes. As part of this compliance, institutions must identify customers who may have a higher risk of being involved in financial crimes. PEP screening helps identify high-risk customers and prevent financial crimes.

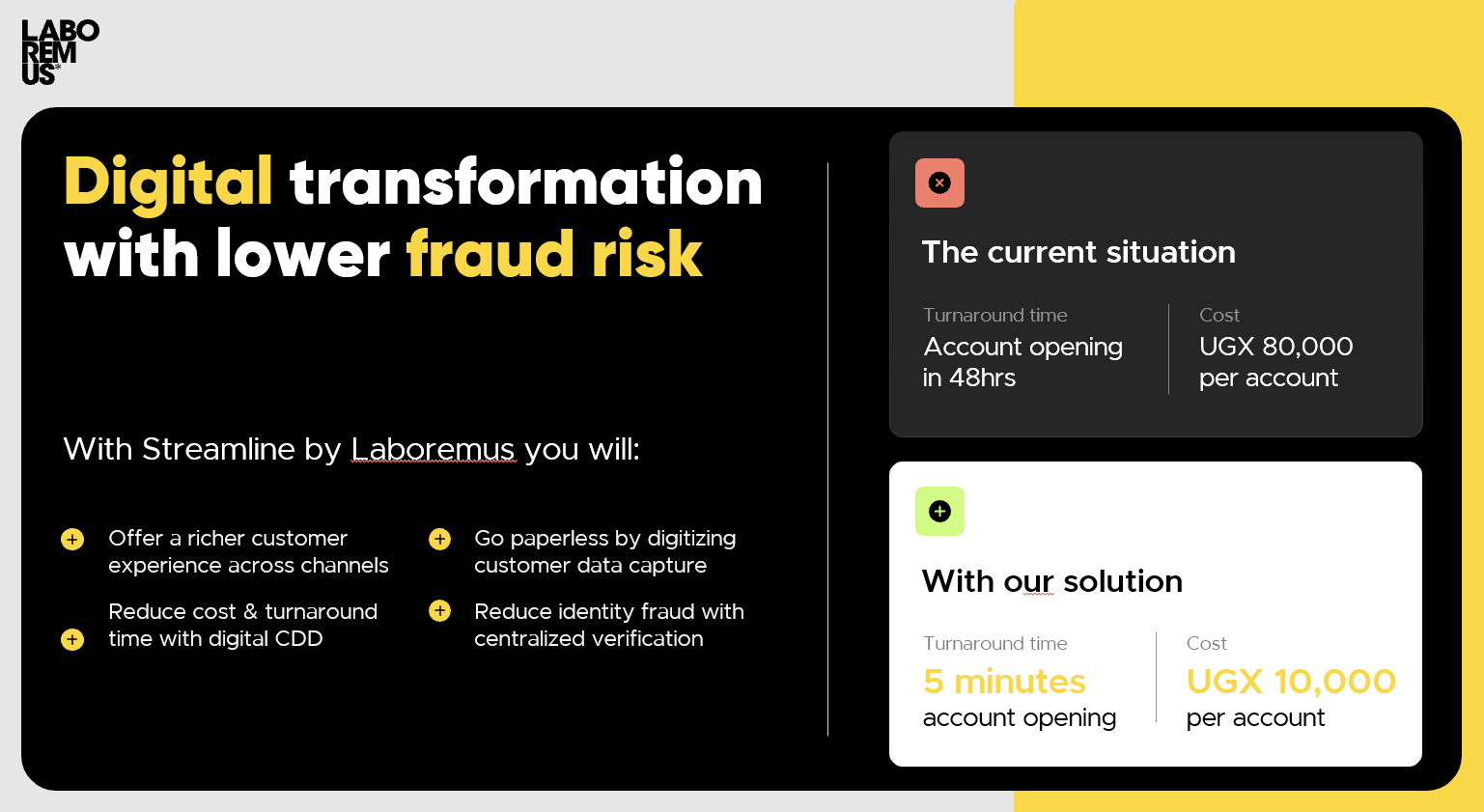

By implementing automated KYB verification, financial institutions can optimise their operations, offer superior experience to their customers and massively reduce their risk to fraud.