Why this choice is harder than it looks

A KYC vendor sits at the centre of a bank or fintech's onboarding, compliance and customer-experience stack. Pick the wrong one and you inherit a problem that touches every customer, every regulator filing and every audit. In East Africa specifically, the question is harder than the global vendor landscape suggests, because the registries that matter (NIRA, URSB, KCCA, NITA-U) are not in the global vendors' catalogues by default.

Below are seven questions to ask any KYC platform before you sign.

1. Are you integrated directly with NIRA, or relying on a scanned copy?

This is the first cut. A KYC platform that checks the customer's National ID against an image of the card has not done identity verification, it has done OCR. A live NIRA integration confirms the NIN is valid, the holder is alive, and the registered details match the application. Anything less is theatre.

2. What is your median check time, end to end?

Customer drop-off on digital onboarding is brutal, and almost always driven by latency. A median check of 30+ seconds will cost you customers. Sub-15 seconds is the modern benchmark when biometric, document, registry and AML/PEP screening run in parallel.

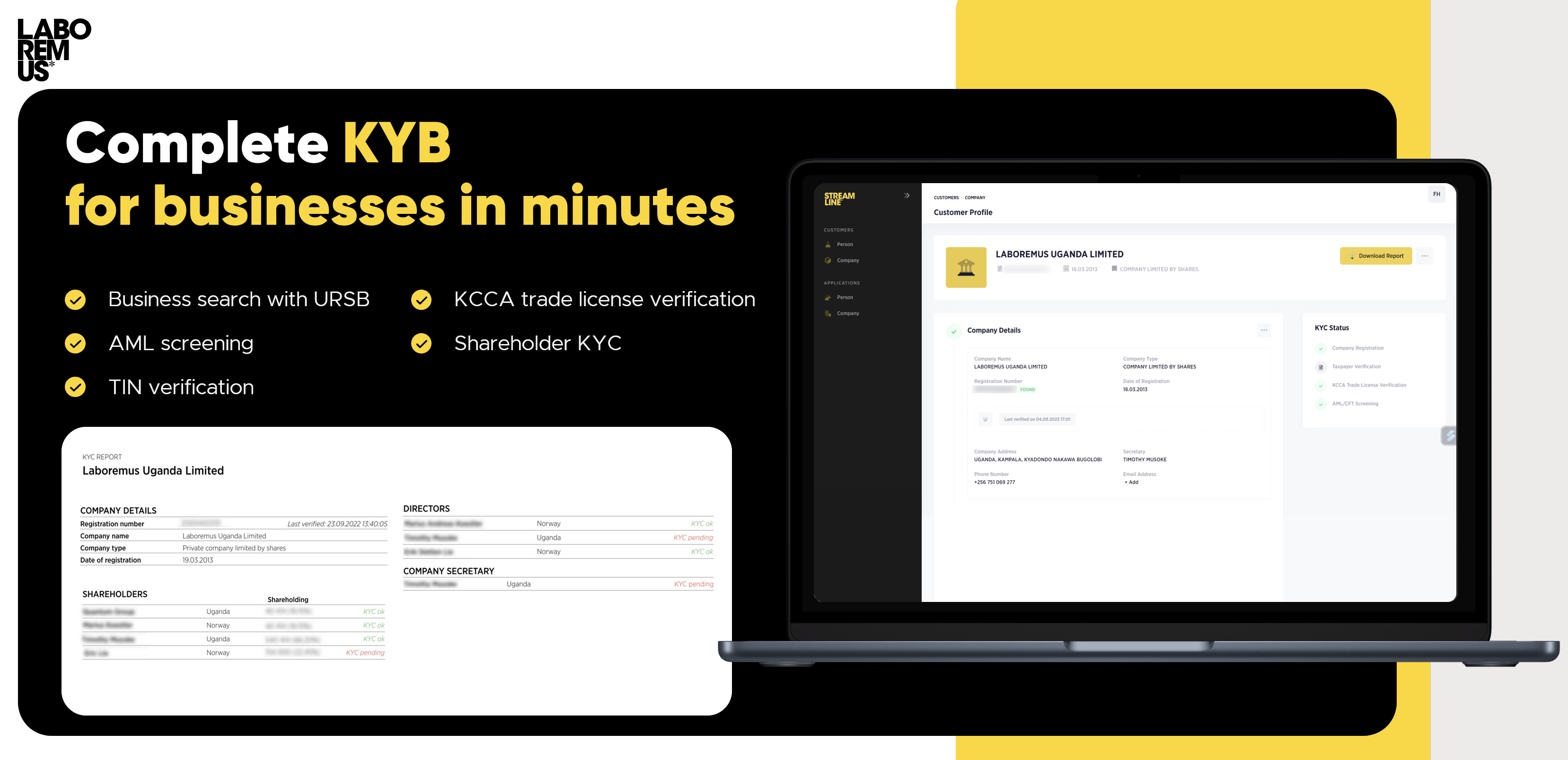

3. Do you cover KYB as well as KYC?

If you serve corporate customers, you need to onboard the business and verify every shareholder. That means direct integration with URSB and KCCA on the business side, and the ability to cascade KYC on each natural-person owner. A platform that does only KYC will force you to bolt on a second vendor, and stitch the audit trail together yourself.

4. Is your audit trail FIA-ready?

Ask the vendor to show you a real KYC report. It should contain every individual verdict, every latency, every screening list hit, every match score and a full chain-of-custody for the operator who ran the check. The Financial Intelligence Authority will ask for these on inspection, they should be one click away, not an engineering ticket.

5. Can we host this on-prem if we have to?

For most institutions, hosted in Azure Africa is fine. For some Tier 1 banks and government-facing institutions, the procurement requirement is on-prem. Ask the vendor early, if they only offer SaaS, the conversation ends there.

6. What does the pricing actually look like?

Per-check pricing dominates the market, but the rate that matters is your effective per-check rate at your real volume, after subscription fees, minimums and registry pass-throughs. Ask for a worked example at your projected volume. A vendor that will not give one is a vendor whose pricing will not survive contact with your CFO.

7. How long until we are live?

Portal-only deployments should be live the same week. A light API integration should be done in 2–4 weeks. A full core-banking integration with bespoke workflows is 1–3 months. If a vendor quotes you 6+ months for any of those, they are scoping you into a custom-build project, not selling you a product.

One more question, off the list

Is the vendor's team in the same country as the customers you are onboarding? A KYC vendor headquartered three time zones away cannot run NIRA outage drills with you in real time. The teams that operate STREAMLINE at Laboremus are in Kampala, the same buildings as the institutions they support.

How Laboremus answers all seven

STREAMLINE is the KYC and KYB platform that 40+ banks, MFIs, SACCOs and fintechs across East Africa run their compliance on. Direct integrations with NIRA, URSB and KCCA. Sub-15-second median checks. FIA-ready audit trail. Hosted on Azure Africa or on-prem. Volume-tier pricing.

If you would like to see STREAMLINE running on your own customer file, the first walkthrough takes 30 minutes.